Calgary Real Estate Market: Q1 2026 Analysis & Spring 2026 Forecast

Something shifted in March.

After two quiet winter months, Calgary's resale market picked up pace in the final weeks of Q1, not dramatically, not in every segment, but enough to signal that spring is arriving with more momentum than the first quarter suggested. If you've been watching the market from the sidelines, wondering whether this is the right time to move, this is a good moment to look at what the data actually shows.

What follows is a plain-language walkthrough of Q1 2026 — month by month, property type by property type — along with an honest assessment of what it suggests about the weeks ahead.

The Full Quarter: Month by Month

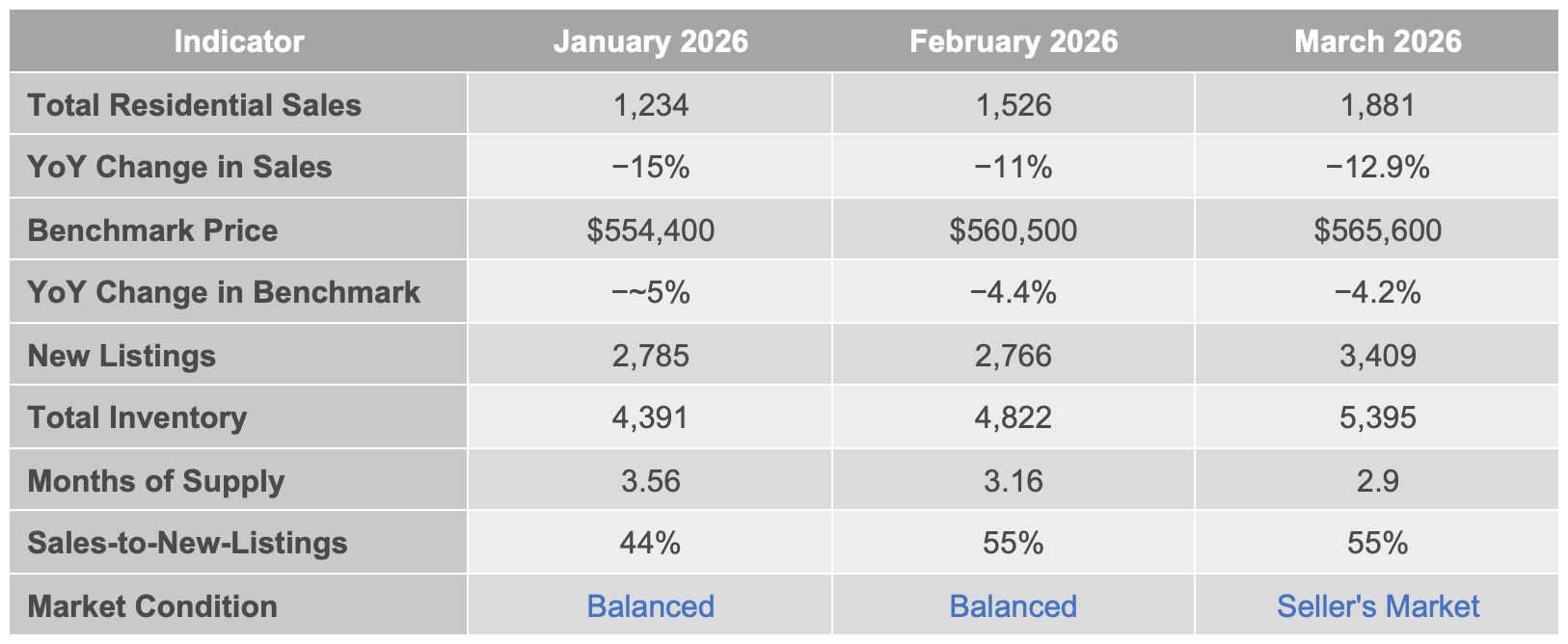

Q1 data from CREB® shows a market that started cautiously, steadied in February, then showed clear signs of seasonal momentum in March. The overall benchmark price — the most reliable measure of a "typical" Calgary home — rose each month of the quarter, from $554,400 in January to $565,600 by March.

Sources: CREB® Monthly Statistics Packages, January–March 2026. WOWA.ca Calgary Housing Market Report, April 2, 2026.

Year-over-year sales declines look significant on the surface, but context matters. CREB® Chief Economist Ann-Marie Lurie noted that January's 15% decline was "in line with typical levels of activity for the month," and that the pullback in apartment and row sales is driving most of the citywide decline, not a broad retreat from the market.

The benchmark price trajectory tells a steadier story. A $11,200 recovery over three months — from a soft January to a stronger March — is a modest but consistent signal of stabilization, not continued erosion.

Where It Really Gets Interesting: Four Very Different Markets

The citywide numbers are useful as a starting point. But the more revealing story is what's happening inside them, because depending on which property type you're buying or selling, you are in a fundamentally different market.

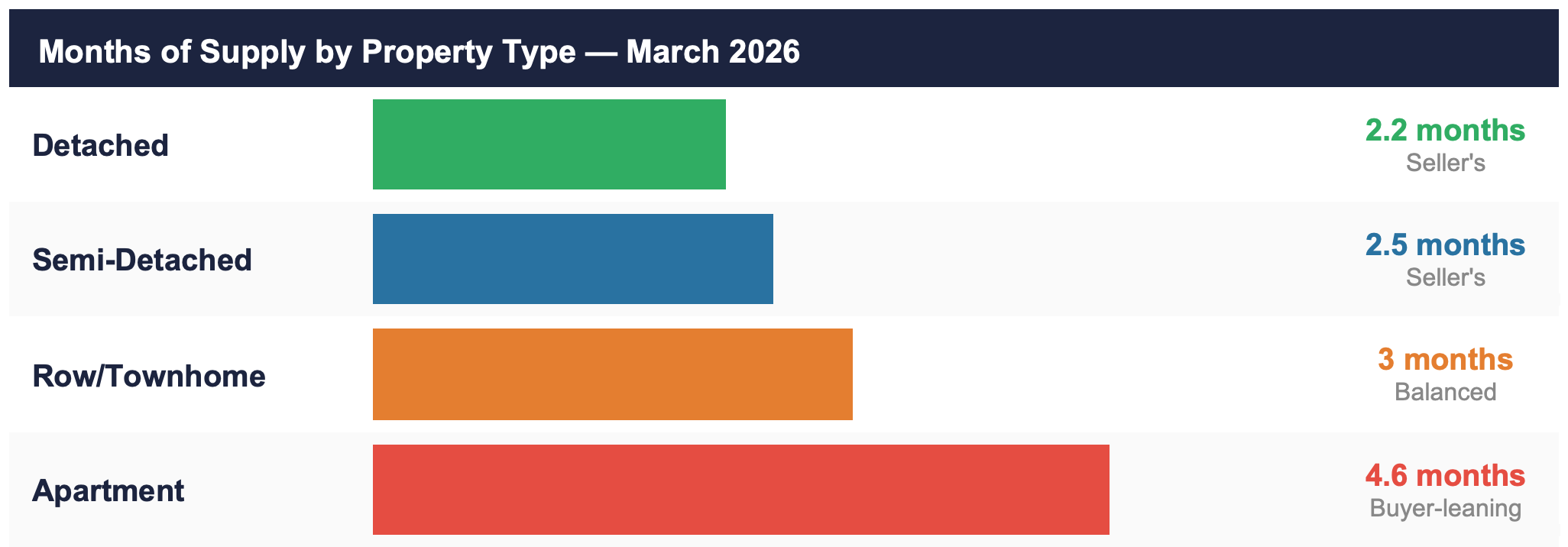

Here's how each segment looked by the end of March:

Sources: CREB® March 2026 Monthly Stats - City of Calgary

Detached — Tight, and Getting Tighter

This is the segment where competition is most real in 2026. With 982 sales, a sales-to-new-listings ratio of 61%, and just 2.2 months of supply, detached homes ended Q1 in clear seller's market territory. The benchmark price of $741,300 is down 3% from last year's peak of $766,600 — but as CREB® noted, tight conditions across most city districts are supporting upward price momentum.

The constraint is particularly sharp below $700,000, where supply is limited and buyer interest remains steady.

"Meanwhile, on the opposite end of the spectrum, the detached market remains relatively balanced in the higher price ranges and continues to struggle with limited supply for homes priced below $700,000."

— Ann-Marie Lurie, CREB® Chief Economist, February 2026

Semi-Detached — The Quiet Out-performer

Semi-detached was the only property type to record year-over-year sales growth in March — up 4.9% to 193 units. With inventory of 480 units and just 2.5 months of supply, conditions are the tightest of the quarter compared to long-term norms. The benchmark price of $686,100 is nearly flat year-over-year (−1%), and month-over-month momentum is positive.

Row and Townhomes — Adjusting, but Not Distressed

At 3.0 months of supply and a benchmark of $423,900 represents a 6.2% year-over-year decline, placing it near the boundary between balanced and seller conditions. Sales fell nearly 20% year-over-year in Q1, reflecting the increased supply choice buyers now have — but the Northeast district is where conditions are softest; most other areas remain relatively balanced.

Apartment Condos — Where Buyers Have the Most Leverage

This is the segment shaped most directly by Calgary's construction boom. With nearly 18,000 apartment units currently under construction and a slowdown in interprovincial migration, the condo market has the most supply relative to demand. At 4.6 months of supply and a benchmark of $300,300 (−9.3% YoY), apartment buyers in 2026 have genuine negotiating room.

That said, a 9.3% correction brings condo prices back toward mid-2024 levels — not a collapse, and still well below comparable units in Toronto or Vancouver.

The Bigger Picture: Rates, Economy, and What's Driving Buyer Behaviour

Two forces are shaping buyer and seller decisions right now.

The Bank of Canada held its policy rate at 2.25% for the third consecutive meeting on March 18, 2026. Most major Canadian banks — including TD, BMO, and CIBC — are projecting the rate will hold at this level through the rest of the year. After two years of dramatic rate changes, what buyers and sellers need most is predictability. The current environment offers that.

On the provincial level, CREB®'s 2026 Annual Forecast projects Alberta's GDP growth at 2.1% — below last year, but still ahead of most other provinces. CREB’s 2026 forecast points to unemployment around 7.4%, which has taken some urgency out of the market. But population inflows into Calgary continue, and the long-term demand picture remains supported by Alberta's relative affordability and employment diversity.

The result is a market that has lost some of its edge, but none of its foundation.

Sources: Bank of Canada, March 18 2026 announcement; CREB® 2026 Annual Forecast Report; CREB® February 2026 Stats Release.

What Spring 2026 Looks Like From Here

Spring is typically Calgary's busiest real estate season, and the Q1 data provides a reasonable foundation for what buyers and sellers might expect as the market enters its peak weeks.

For Buyers

Competition is returning in detached and semi-detached. With months of supply at 2.2 and 2.5 respectively, serious buyers should be prepared and pre-approved before viewing.

Condos and row homes offer the most negotiating room. Buyers in these segments have more time, more choice, and more pricing leverage than at any point since 2020.

Rates are holding steady, not falling. If you are waiting for mortgage rates to drop before buying, the current consensus among economists suggests that window has likely passed for this cycle.

Spring listings are coming. As inventory typically rises through April and May, buyers may have marginally more selection — but in the detached segment, well-priced homes below $700,000 are still moving quickly.

For Sellers

Pricing strategy has never mattered more. Overpriced homes are sitting. The March data shows that 3,409 new listings came to market while 1,881 sold — meaning new listings outpaced sales in March. Correct pricing from day one is essential.

Detached and semi-detached sellers remain in a relatively strong position. With supply in these segments still below 3 months, well-prepared and well-priced homes can still achieve strong results.

Condo sellers need a different approach. In a buyer-leaning segment with 4.6 months of supply, presentation, price credibility, and marketing quality matter more than they have in years.

Spring is still your best window. Historically, the highest buyer activity in Calgary occurs from April through June. If you are thinking of selling in 2026, this is the time.

A Note on Sources: All statistics in this article are drawn from CREB® official monthly statistics packages for January, February, and March 2026, supplemented by WOWA.ca (updated April 2, 2026). Macroeconomic data sourced from the CREB® 2026 Annual Forecast Report (Ann-Marie Lurie, Chief Economist), Bank of Canada March 18 2026 announcement.

Thinking about buying or selling in Calgary this spring? Let's talk through your specific situation — no pressure, no obligation.

📞 (403) 383-3099 • verona@veronahomescalgary.ca • veronahomescalgary.ca